As Financial Literacy Month draws to a close, let’s revisit some financial lessons of the past. What did you learn about money while growing up, and what do you hope to impart to the next generation? Here is a start:

- A penny earned is a penny saved. (Save, save, save!)

- Money doesn’t grow on trees. (Work to earn money)

- You have to spend money to make money. (Invest)

- You get what you pay for. (The value of goods)

These are all great lessons and important ones, but one that should definitely be on your list is to only spend what you earn (or have).

Why is it important to limit what we spend? If we go overboard with expenses, we rely on borrowing from others. Another word for borrowing money – debt. That not only puts added stress on us to pay back what is owed, it causes a cycle to start. After all, we borrowed once, what’s a little more? And remember compound interest and how awesome it is to watch money multiply in value? It works for credit card companies too. That 10% or 15% or however much interest that we could have been earning on our money is what credit card companies make on us through credit card debt. So let’s just avoid it all by sticking to what we can afford.

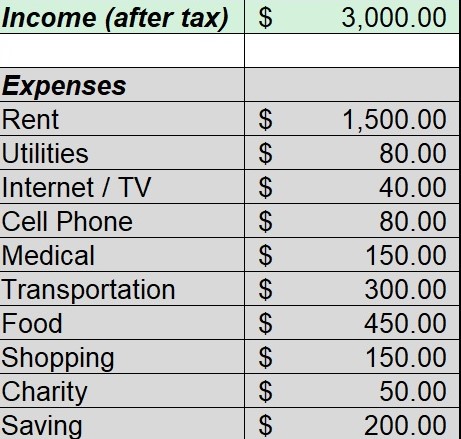

How do we keep track of our spending with so many expenses? That brings us to the topic this month: Budgeting. A budget is a plan for spending. Essentially, add up what you earn or take home every month and subtract spending in each category. We can use the following budget as a case study.

What observations do you have of this sample budget? A few areas to note:

- Expenses add up to income, meaning no overspending. Well done!

- This budget includes saving as a line item, so that it’s not an afterthought. Even better if that money is directly deposited into a savings account and/or investment plan!

- Saving could use some improvement, perhaps increasing from 6.7% to 10% or 15% instead.

Creating a budget is a good start, but sticking to a budget is what really matters. A plan only works if you follow through, right? One way to stay within budget is to give yourself a CASH allowance for categories like shopping or food, so you only spend what you have in cash each month. Another way is to track your spending through free tools offered by your financial institution.

As life changes occur, remember to modify your budget accordingly. It may mean cutting certain costs to allow for new ones. And beware of lifestyle creep. Making more money does not mean getting fancier things or dining out more if you haven’t increased your savings as well. And above all, regardless of whether you make a five- or six- or seven-figure income, only spend what you earn!